Homeowners And Commercial Property Owners To Face Tax Increases Over Six Percent

By Robert Thomas

Despite approving the 2022 - 2023 Operating Budget before Christmas - with a 5.45 percent tax increase - Executive Committee was told there were still a few lumps of coal to give out as the spirit of Grinch seemed to linger in the corridors of City Hall.

On Monday Executive Committee was asked to establish the mill rate for 2022.

The mill rate, when used in a formula which includes a provincial mill rate factor (based on the class of property), plus a property assessment, is used to determine the tax rate for all properties in the city.

The end result of the discussion was the actual property tax increase for residential property is 6.4 percent and for commercial properties it is 6.56 percent from the originally announced 3.56 percent.

The reason for the 3 percent increase for Commercial properties from the original Budget amount of 3.56 percent is due to Executive deciding to collect taxes lost from successful tax appeals within the Commercial property class.

The Committee decided against asking all taxpayers to share the cost of incorrectly assessed commercial properties or as in 2021 use the Accumulated Surplus to pay for successful commercial tax appeals.

At the present time the Accumulated Surplus - a fund where unspent budget funds (such as unused snow removal funds) are deposited - has a balance of $856,890.

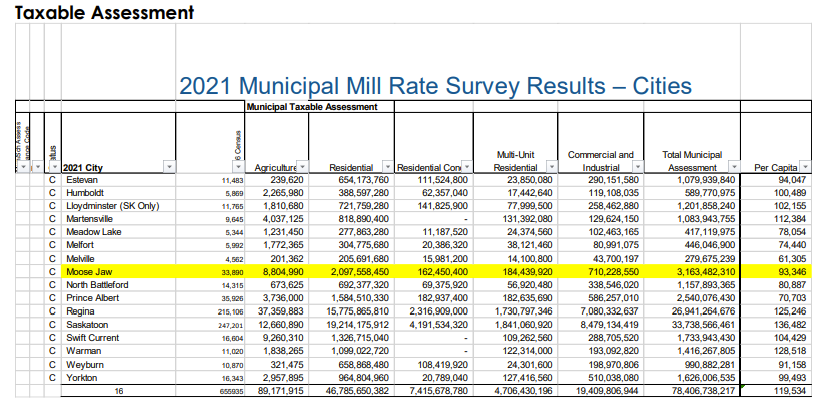

Discussion - First The Statistical Comparison

Beginning his presentation to Executive Committee Finance Director wanted to highlight where Moose Jaw sat for taxes on a per capita basis compared to other cities in the province.

On a per capita basis Acker pointed out Moose Jaw has a mill rate that is seventh lowest versus other cities in the province with a 93.346 per capita rate with $3,163,482,310 total municipal assessment.

Moose Jaw’s per capita mill rate compared to other Saskatchewan cities - City of Moose Jaw graphic

Acker went on to point out municipal taxes generated per capita were the fourth lowest versus other cities in the province.

Taxes generated per capita in Moose Jaw versus other Saskatchewan cities - City of Moose Jaw graphic

The graphs also point out Moose Jaw has the fifth lowest residential taxes in Saskatchewan’s 16 cities.

Comparison of Moose Jaw’s taxes versus other Saskatchewan cities - City of Moose Jaw graphic

The charts provided also show when it comes to commercial taxation Moose Jaw is the sixth lowest amongst Saskatchewan’s 16 cities.

It needs to be noted there are critics of the per capita approach they believe the per capita rate is irrelevant and shows nothing. They prefer a comparison showing taxable rate per a set amount of assessment valuation.

Another concern critics raise is the per capita method does not factor in or show the amount of economic activity in the centres in order to be able to pay for higher tax rates.

Discussion - Mill Rate Factors

“Mill rates factors are one of major tax tools. It allows us to increase or decrease taxes in the various assessment classes,” Director of Finance Brian Acker told Executive going on to ask the Committee to approve changes to the mill rate factors to allow for issuance of the 2022 tax notices.

The first property class discussed was arable or farm land within the City of Moose Jaw.

Acker asked the Committee to tax agricultural lands at the same rate as charged by the RM of Moose Jaw.

“The City has had a long standing policy to tax that land, which is within City limits, at the same rate as the RM of Moose Jaw,” he said.

Last year Council passed a motion agreeing with the long standing policy.

Residential and Commercial Tax Gap

Acker told Executive in 2018 Council looked at the tax gap - the amount of taxes charged for the same amount of assessment in the residential and commercial/industrial property classes - between residential and commercial properties and had developed a policy to reduce the gap.

The policy became known as tax sharing which would slowly see the gap eliminated by incrementally shifting the tax burden from commercial to residential properties.

The issue was known as Tax Fairness and was part of a major campaign by the business lobby group the Canadian Federation of Independent Businesses (CFIB).

When Council adopted the policy to reduce the property tax gap in 2018 former Councillor Don Mitchell voted in favour of the gradual approach but also spoke out about Tax Fairness and the how the “tax shift” placed an increasing burden on many economically disadvantaged homeowners. Mitchell asked for tax fairness for homeowners of lesser means.

“At that time it was 2.35 times so a commercial property assessed at the same level as a residential property paid 2.35 what a residential property was. City Council saw that as an issue. Certainly an impediment to economic development and what they did was adopt a policy that is slowly transitioning that tax gap,” he said.

“It is based on assessment rather than some arbitrary scary sort of calculations that were done in the past.”

Chart showing the reduction of the Commercial to Residential Tax Gap from 2021 to 2022 - City of Moose Jaw graphic

The mill rate factor for 2022 is 1.3681 versus 1.3931 in 2021. The final mill rate factor for businesses in 2022 will be 1.412 once property assessment appeals losses are factored into the amount.

For residential property owners the mill rate factor increased from 0.774 in 2021 to 0.7810 to reflect the shifting of property taxation or tax sharing by homeowners.

“It is slowly causing that tax gap to go down,” Acker said, adding “it is a significant decrease.”

The tax gap between commercial and residential properties in 2018 was 2.35 times per the same assessed value whereas in 2022 it is 1.89 the same assessed value.

In later questioning Councillor Heather Eby asked Acker what is the acceptable assessment difference between commercial and property assessments to which he replied they should be equal.

“In a perfect world there would be no gap. They would be the same,” Acker said in answer to Councillor Eby.

Appeal Losses

Property tax appeal losses for improperly assessed commercial property continues to be a problem for the City.

The majority of the appeal losses are from commercial properties with 434 appeals in the last five years. The majority or 75 percent of successful appeals of improper property assessments were conducted by professional appeals assessment agents.

Out of the appeals the City reached an agreement to enter into an adjustment with 87 appeals. There were 64 appeals withdrawn.

The Board of Revision threw out 156 appeals and a further 156 appeals were sent to the Saskatchewan Municipal Board to be further appealed.

In 2021 the City sustained losses in assessed values of $24.75 million for improperly assessed commercial properties.

“It certainly is significant. We did make an allowance last year for five percent so it did come in a little bit below what we had estimated. But certainly significant as the total tax losses amount to about $358,000.

Acker said the loss of $358,000 breaks down to a permanent loss of $154,000 for the 87 agreements there had been assessment errors for commercial properties. Plus there is $208,000 in losses which may be temporary as they are currently being appealed.

“We may win those at some point but until we do until which has been two, three or more years down the road we will suffer that as a permanent loss each year until that is a win for the City.”

Acker said there was three options to make up for the commercial assessment appeals losses - generate it from all commercial businesses, use the Accumulated Surplus (the option employed in 2021) or an overall mill rate increase for all property classes.

He said Administration recommended the appeals shortfall be made up in a revenue neutral manner and that the burden be borne by commercial/industrial properties alone.

“If we knew we were going to have this 3.15 percent loss in our commercial sector through appeals we would have taken that into account at that time,” said in defending Administration’s recommendation.

“In effect that would put it up to a 6.56 percent increase (for commercial properties) making it almost identical for the residential for the year,” Acker said.

In 2022 the estimate for commercial losses is 1.7 percent which can be covered by Council approving a five percent cushion in 2021 by utilizing the Accumulated Surplus.

Committee’s Decision

Councillor Eby said it made sense to her to accept Administration’s recommendation although in the past it may not have been what other Committee members were prepared to accept.

There was no further discussions before the vote.

In a 6 - 0 vote Executive Committee approved:

agricultural lands will be taxed at the same rate as lands in the RM of Moose Jaw once that rate becomes available

the policy of reducing the tax gap between commercial and residential property will continue

residential property taxes will increase by 6.4 percent

assessment appeals losses from commercial properties will be made up by all commercial properties resulting in a 6.56 percent tax increase.

Councillor Crystal Froese was absent.